Sales growth to come from both strong export demand and domestic population growth

Meat products export growth is expected to rebound in 2023 after a weaker 2022, amid risks that demand weakens. Pork exports to China are expected to be limited, given their herd rebuild, while a weaker global economy could dampen the outlook for export growth.

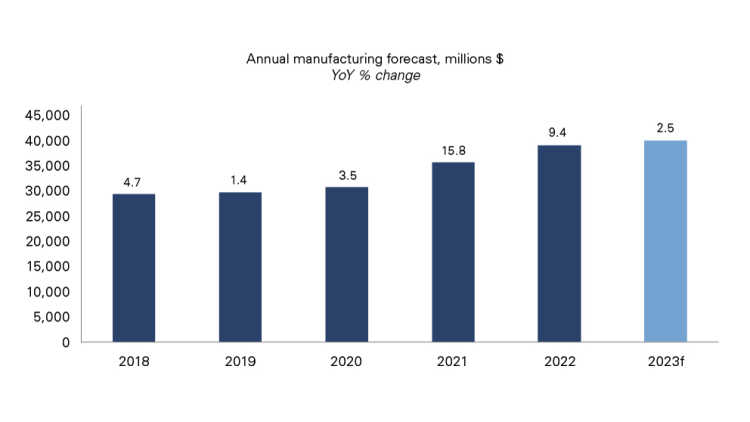

FCC Economics projects sales from meat product manufacturers to increase 2.5% in 2023 (Figure E.1).

Figure E.1: Meat product sales are expected to increase 2.5% in 2023

“Consumers eating cheaper cuts of meat also negatively impact margins, as higher value cuts are sold at generally higher margins”

The outlook for domestic meat consumption is also uncertain. Inflation will likely encourage consumers to choose cheaper cuts of meat and other protein sources. According to the Organization for Economic Co-operation and Development’s (OECD) 2022 outlook, Canadian per capita beef consumption is forecasted to decline 1% in 2023 compared to global consumption projected to be flat. Domestic per capita pork consumption is forecasted to be flat and to rise 2% YoY globally.

Canada’s per capita chicken consumption is forecasted to rise 1% and be flat globally. Canada’s meat sector volume growth will have to come from population growth. We expect manufacturing price inflation in 2023 to remain roughly in line with 2022.

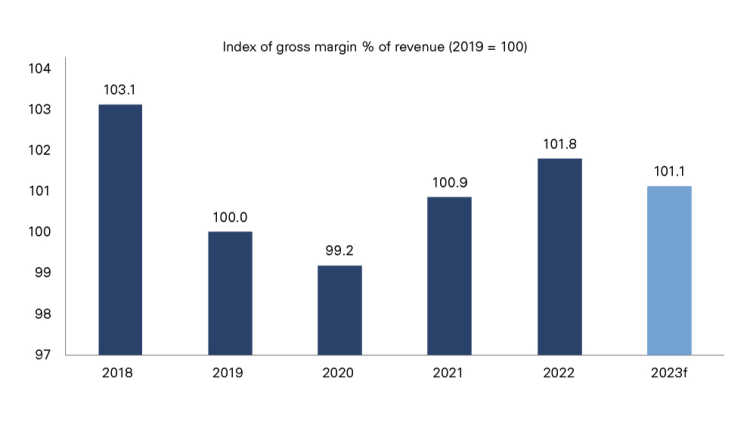

Margins are forecasted to decline in 2023, continuing the weakness in Q4 2022 (Figure E.2). Higher prices for live animals are the leading cause of expected margin erosion. Consumers eating cheaper cuts of meat also negatively impact margins, as higher value cuts are sold at generally higher margins.

Figure E.2: Margins increased for a second straight year in 2022, led by beef

Sources: FCC Economics, Statistics Canada

How we got here: Rebound in restaurant sales

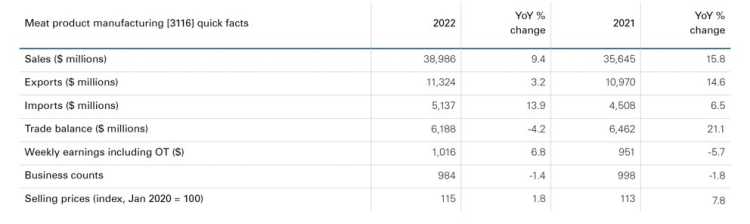

Meat product manufacturing sales increased over 9% YoY in 2022 (Table E.1), largely due to stronger domestic sales (up 12%), led by foodservice growth. Prices were stable compared to many other industries, rising 1.8% YoY. Canadian retailer prices rose 8.1% in 2022. The discrepancy was largely the result of delayed price increases after manufacturing prices rose 12% in 2021. Nonetheless, Canadian consumer meat prices rose less than in the U.S. and abroad. According to the UN, global meat prices rose 10.4% YoY in 2022.

Table E.1: Sales growth driven by increased domestic consumption

Source: Statistics Canada

Domestic sales picked up as export growth slowed. China, which represented 5% of all Canadian beef exports in 2021, banned the import of Canadian beef in late 2021, resulting in those exports falling towards zero in 2022. Overall pork export values declined 6% YoY in 2022, again led by China, where Canadian exports declined 48% YoY. Increases in the U.S. and Mexico partially offset that decline.

The story was mixed for domestic grocery volumes. According to Nielsen IQ data, pork was a bright spot, with volume sales growing over 1% YoY. But meat product grocery volumes declined 3% in 2022, with beef and veal volumes declining over 4%. Higher chicken retail inflation (due to the impact of Avian Influenza disrupting supply) generated a decline in chicken volume sales smaller than beef.

2022 meat manufacturing industry profitability was mixed. Margins were healthy across all three major proteins but experienced notable weakness at the tail end of the year. Raw chicken prices rose 11% YoY in 2022 after rising 13% YoY in 2021. Cattle prices rose 16% YoY after rising 9% YoY in 2021, while hog prices rose 7% YoY after rising 29% YoY in 2021. Canadian manufacturers managed higher costs and prevented retail prices from climbing even more than observed at retail.

Bottom line

The past few years have entailed a balancing act for meat manufacturing. Canadians still have strong preferences for meat amid a desire to diversify their food basket and alternatives that have emerged.

Labour challenges in the industry led to higher wages and strengthened benefits packages to attract new employees, with industry employee earnings growing over 7% YoY.

The number of meat manufacturing businesses declined by 14, with the reduction of small and independent manufacturers.

The year ahead looks bright if a significant slowdown of the Canadian and global economies can be avoided: inflation is expected to subside, and meat sales look robust, driven by foodservice, convenience meat products and exports.

In our November 2025 issue, the DOJ beef sector investigation, McDonald’s becomes farmers big ally, Trump angers U.S. farmers, Canada Mexico agri-food deal, Ontario’s finest butcher, Beef perception shift, Global beef sustainability, and much more!

")