")

2020 Outlook: Canada’s Red Meat Sector

FCC Ag Economics helps you make sense of these top economic trends and issues likely to affect your operation in 2020

by Leigh Anderson, Senior Agricultural Economist – Farm Credit Canada (FCC)

African Swine Fever’s disruption of livestock and meat markets Trade tensions’ influence on agri-food markets Robust global and domestic red meat demand U.S. growth in beef and pork production Global economic impact of coronavirus

Profitability for the red meat sector is expected to be positive in 2020 due to robust export demand. The decline in global meat protein supplies caused by African Swine Fever (ASF) remains a story to watch in 2020. The U.S. and China agreed to a phase one deal that could raise North American prices. But the implementation of the agreement remains vague. The supply response of U.S. livestock producers will also determine livestock prices. In short, the volatile environment of 2019 is expected to extend throughout 2020.Futures markets suggest prices for most Canadian cattle and hogs will remain around their five-year average, but higher than the 2019 average.

“We expect continued robustness as beef and pork remain competitive from a price standpoint relative to substitutes”

Table 1. Livestock prices projected to be higher than last year

Sources: Statistics Canada, USDA, CanFax, CME Futures and FCC calculations.

Profitability for the cattle sector is trending up

Profitability in the cattle sector is expected to be slightly above break-even through 2020. Strong demand for feeder cattle will support profits for cow-calf operators, while feedlot operators will see improved profitability compared to 2019.

Live Canadian cattle prices averaged C$150 per cwt for fed steers in 2019, generating a 10.8% estimated increase in receipts from 2018. We’re projecting prices for Canadian fed steers to average C$148 per cwt in Ontario and C$155 per cwt in Alberta in 2020. Similarly, prices for Canadian feeder cattle (550 lb and 850 lb) are expected to be in the C$218 – C$228 range. Eastern Canadian bids for cattle are projected lower as the industry deals with wider basis levels due to a decline in slaughter capacity. U.S. beef production grew 1.0% in 2019, significantly lower than the 3.1% projected at the beginning of the year by the USDA. Projections call for U.S. beef production to climb 1.2% in 2020.

Our preliminary estimate indicates Canadian beef production grew 2.8% in 2019, as more cattle were fed and slaughtered in Canada in 2019. Canadian packer utilization rates continued to be strong. We estimate that the ratio of beef slaughtered (in federally inspected facilities) relative to capacity increased in the second half of 2019: 94.8%, up from 90.5% during the first six months, and well above the five-year average of 86.5%.

Several factors explain strong packer utilization:

Robust demand for beef coupled with strong processing margins Beef processing plant closures in eastern Canada A major U.S. beef processing plant was idle for a few months Higher imports of U.S. live cattle into Canada Increased culling rates in Canada due to unfavourable weather conditions

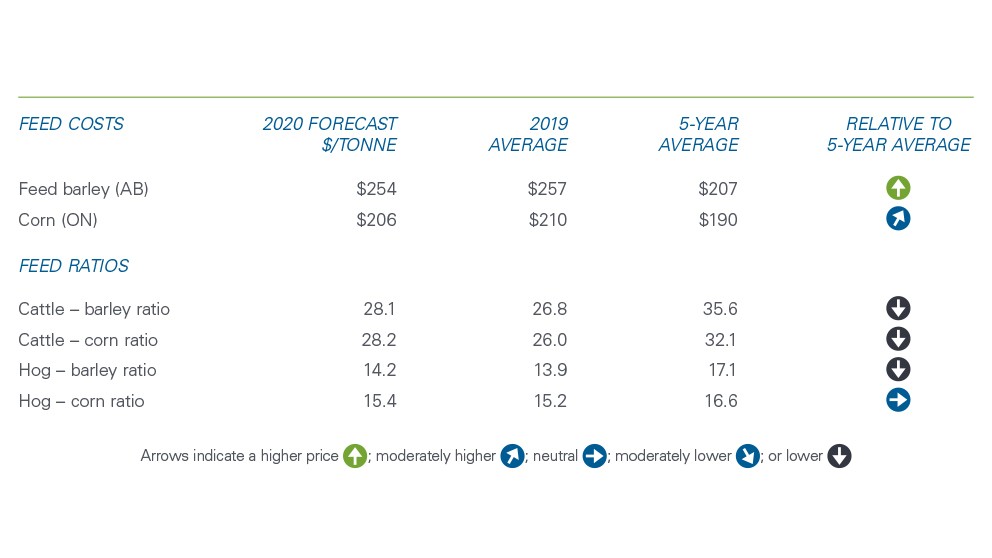

We expect the Canadian processing sector to continue operating at high capacity as the January 1, 2020, cattle-on-feed in Canada was estimated to be 10.7% higher compared to January 1, 2019, and 20.4% higher than the five-year average.Our grains and oilseeds outlook for 2020 suggests average feed prices will be relatively similar to last year. While unfavourable weather conditions increased feed costs in 2019, both corn and feed barley prices are expected to be slightly lower in 2020. The combination of slightly weaker feed prices, along with slight improvements in livestock prices, means improvements in the feed ratios for cattle and hogs supporting profitability in 2020. Yet, profitability is expected to remain below the five-year average.

Table 2. Profitability trending up in 2020 on higher revenue projections and similar feed costs

Sources: Statistics Canada, USDA, CanFax, CME Futures and FCC calculations

Hog prices supported by ASF, yet tariffs and large U.S. production lower upside

The 2019 variability in hog profits is expected to carry into 2020. We’re forecasting 2020 average Canadian hog prices between C$78 – C$81 per cwt, a 3.4% increase from 2019. U.S. pork production grew by 5.0% in 2019, and the USDA projects will increase by 4.5% in 2020. The continued expansion of the U.S. hog sector has raised concerns relative to the U.S. slaughter capacity. The good news is that the larger U.S. pork production is more than offset by the strong demand arising from the ASF-led decline in Chinese pork supply.

The 2019 temporary export restrictions into China likely explain how pork slaughter capacity stood at 85% in 2019, slightly below the five-year average of 88%. As U.S. hog slaughter approaches capacity throughout 2020, we expect Canadian slaughter utilization will rise. Boosting Canadian exports to China and other Asian countries will be crucial in 2020 to supporting the red meat sector. U.S. pork exports to China increased in 2019 despite China’s retaliatory tariffs on U.S. pork. Reducing tariffs on U.S. hogs into China could go a long way in supporting lean hog prices in North America.

Trends to watch in 2020

1. Food preferences shift, but domestic demand for red meat remains robust

Beef retail prices grew 3.5% in 2019 compared to 0.7% for pork and 3.0% for chicken. The global gap between pork supply and demand is expected to lift prices for animal proteins. Although retail sales of tofu, meat and dairy alternatives climbed by 25% in 2019 (Nielsen data), and are expected to keep growing, they’re still small compared to sales of animal proteins.

The FCC Canadian beef and pork demand index remained strong in 2019. We expect continued robustness as beef and pork remain competitive from a price standpoint relative to substitutes. Convenience, solo-eating, snacking and quality will continue impacting food purchasing decisions.

2. China’s ability to rebuild its hog herd

The FAO estimated that China’s pork production declined at least 20% in 2019. Various forecasts call for at least a further 15% decline in 2020, creating a potentially large gap between demand and supply. China’s pork retail inflation reached over 100% YoY in 2019 and pork imports are expected to increase considerably in 2020. Despite ongoing consolidation, Chinese hog operations are rebuilding. A faster-than-expected rebuild of the Chinese hog herd could lead to demand for red meat being below expectations. A vaccine to ASF developed in the U.S. was recently proven successful, yet it’s unknown how fast it can be deployed commercially.

China’s overall impact on global agricultural markets cannot be understated. Consider these statistics: China consumes 27% of all global meat, with 62% of China’s meat consumption being pork. Historically, China only imported 3% of its pork requirements, given its large production capacity. The pace of the rebuild is essential when anticipating the impact of ASF in demand for red meats.

3. China-U.S. phase one trade agreement can have mixed outcomes for Canadian livestock producers

China agreed to import an additional US$32B of ag products from the U.S. over the 2017 import levels in 2020 and 2021. But here’s the caveat – purchases will be based on market conditions, so it’s unclear how binding purchase commitments will be.

Removing the Chinese tax on U.S. pork exports could lead to a considerable price gain for live hogs. The agreement also includes harmonization of trade rules in the beef sector that could ultimately be extended to Canadian exporters.

But not everything in the agreement is positive. It can leave Canadian exporters out of the profitable Chinese market and scrambling to fill demand coming from markets that the U.S. exporters desert.

4. The resilience of the global and Canadian economies to be tested

Trade tensions weighed on the global economy in 2019, which is estimated to have grown at 2.9% in 2019, its weakest performance since 2008-09. Many central banks (led by the U.S. Federal Reserve) proceeded to lower interest rates as insurance against a possible global slowdown. The International Monetary Fund (IMF) projects that economic growth will rebound to 3.3% in 2020, but only if trade tensions continue to ease. We expect one cut in the overnight rate for 2020 to support the resiliency of the Canadian economy.

The loonie gained value against the U.S. dollar in 2019, starting the year under US$0.74 to finish just under US$0.77. The momentum carried into 2020. Uncertainty should be a major theme of global financial markets in 2020, and we project the loonie to return towards the US$0.75 level in 2020.

5. Coronavirus outbreak can weaken the demand for meat

Navigating the red meat market is complicated enough amid ASF and global trade tensions. Throw in the spread of the novel coronavirus, and the situation gets complicated, fast. Financial markets have reacted promptly in fear that a widespread and global outbreak could slow world economic growth. Red meat consumption is a function of global income. An income decline could weaken demand for proteins in emerging markets and shift food purchasing patterns (like fewer restaurant visits).

6. Market access for Canadian red meat exports expands

Implementation of the Canada-U.S.-Mexico Trade Agreement (CUSMA) is expected in the second half of 2020. While market access under CUSMA remains unchanged, ratification of the agreement brings certainty.

The CETA and CPTPP trade agreements will each be in year 3 of implementation in 2020, opening opportunities for diversification. For instance, the value of beef and pork exports to the EU both increased by over 50% in 2019, yet export volumes remain low. Exports to Japan increased by 68% and 11% respectively in 2019. The U.S. established its agreement with Japan, lowering tariffs in sync with CPTPP members starting January 1, which is likely to make the Japanese market more competitive for Canadian meat products in 2020.

Our November 2025 Issue

In our November 2025 issue, the DOJ beef sector investigation, McDonald’s becomes farmers big ally, Trump angers U.S. farmers, Canada Mexico agri-food deal, Ontario’s finest butcher, Beef perception shift, Global beef sustainability, and much more!